This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Unlike big commercial banks, most public banks (and all California public banks under state law) will be nonprofits and use their earnings from loan interest and fees to reinvest in local economies and large-scale community-wide projects. Instead, public banks partner with local banks to expand community-driven impacts.

To ensure mutualism thrives in the next generation, communities need laws, regulations, practices, and capital markets that encourage solidarity and investment outside of any given silo. CDFIs should be expanded to include a wider range of mutualists like unions, cooperatives, mutual banks, and mutual insurance companies.

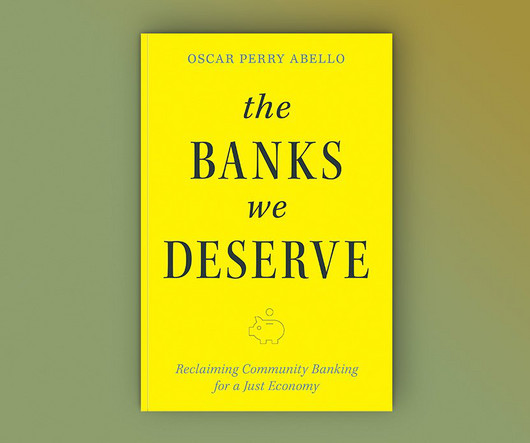

Oscar Perry Abello: In my work as an economic justice correspondent at Next City, I had written all these stories about credit unions, community banking, and CDFIs [ CommunityDevelopment Financial Institutions ]. The local bank has insured FDIC deposits. It has] FDIC insurance just like a regular bank.

Image credit: Ian Nicole Reambonanza on Unsplash This is the fourth article in NPQ ’s series titled Building Power, Fighting Displacement: Stories from Asian Pacific America, coproduced with the National Coalition for Asian Pacific American CommunityDevelopment ( National CAPACD ). How does a refugee community organize itself?

The conference brings together hundreds of community activists, government officials, and bank communitydevelopment officers. Community Reinvestment Strengths and Shortfalls NCRC was formed in 1990 to defend the 1977 Community Reinvestment Act , a law created to undo the structural racism embedded in redlining.

Make sure there are no roadblocks in place preventing non-profits from acquiring services or setting up systems in financial markets, including the insurance markets. The State Auditor office is responsible for insurance regulation and securities fraud prevention. Foster public/private partnerships where possible.

Image Credit: Daniel Xavier on pexels This is the fourth article in NPQ ’s series titled Owning the Economy: Stories from Latinx Communities. How does a small Latinx community organize itself to support homegrown businesses? DevelopingCommunity Leadership Entrepreneurs play a critical role as community builders.

This makes it easy for predatory developers to buy one of the shares from an heir—say, a sibling who wants to sell the property—and then use their influence to force the sale of the entire property so that it can be developed. Without being able to prove ownership via a clear title, then, heirs can lose their home.

The false belief that a person can leverage hard work and talent to pull themselves and their family out of poverty should they only try is a pervasive story that has shaped our culture and laws. The US social safety net consists of Social Security, Medicare, Medicaid, unemployment insurance, and welfare programs.

Colorado’s Story Colorado is home to some of the country’s most favorable cooperative laws. Impact investment and non-bank financing from communitydevelopment financial institutions also remain limited. Developing Professional Supports: Streamlining handoffs and communication is essential to speed conversions and reduce costs.

Job Title: Community Response Program Manager Department: Community Response (CR) Reports To: Program Director FLSA Status: Non Exempt, Full time (40 hrs/week) Compensation: $66,560 – $82,243 annually ($32/hour – $39.54/hour) Position Summary The Community Response team is a critical part of ending violence in our community.

23 Such university developments simultaneously raise property values and contribute little to public services. The most embarrassing edifice to this type of land scheme is the State Farm Insurance regional headquarters that sits on ASU land.

Image credit: AmnajKhetsamtip on iStock Communitydevelopment financial institutions (CDFIs) have emerged as pivotal players in bridging financial gaps in underserved communities. An executive order (14238)calls for reducing the CDFI Fundto the minimum presence and function required by law.

We organize all of the trending information in your field so you don't have to. Join 27,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content